Welcome everyone, to a new series offering explanations on concepts/ideas/terms that are used in the property industry, by an intern with zero background in the property industry. Yep, you read that right.

In this series, I’ll be doing my best to explain these complex terms as simply as I can so that you can best understand it too. If you’re keen on learning more about the property industry, let’s go on this journey together. Welcome to the What Are They (WAT) series, by the Mortgage Noob in Mortgage Master.

Foreword from author:

Hey good lookin’, hope you’re having a fine day today. The tone I used for this piece is kind of a continuation from the previous article, simply because refi and repri are so often compared against one another, so it’d be best if new readers have some sense of what refinancing is first. Till then, enjoy the article. Mad love, take care, be a good person.

Good morning/afternoon/evening whenever you’re reading this.

Like the foreword said, this piece on Repricing is a Subsequent WritingArticle (shoutout to Borat fans) from the previous article of Refinancing, so if you read that, Welcome Back!

If you’re new here, Welcome! Back!

But if you’re familiar with the aforementioned article, I mentioned Repricing a couple of times. I’m so sorry to my fellow noobs because I know that must have hit you like a ddu-ddu-ddu and you might have been left confused, but I had to include it because Repricing and Refinancing are basically siblings

How Repricing works

Maybe the term siblings isn’t quite accurate. What I mean to say is that they’re twins.

Repricing exists to save you money by offering lower interest rates, same as Refinancing.

The core reason you should Reprice is to lower your costs of your property, same as Refinancing.

Repricing still has a lock-in period with exorbitant thereafter rates, same as Refinancing.

But enough of Repricing and Refinancing being Related, they are still different concepts because of 1 major distinction.

What is Repricing?

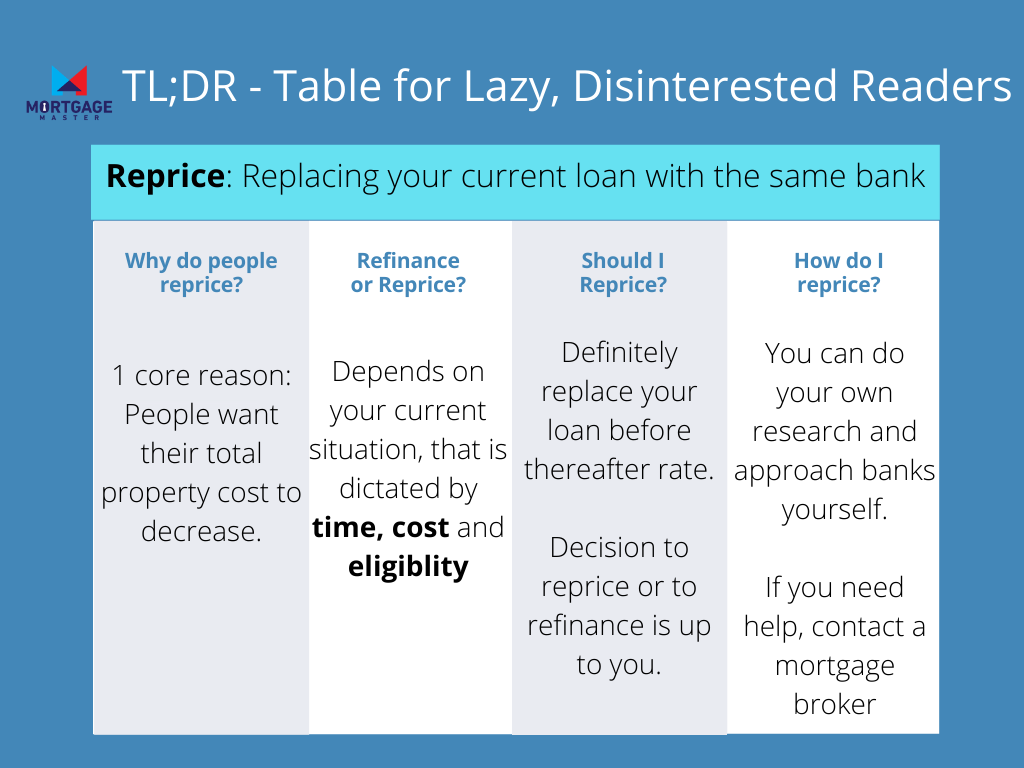

Repricing refers to replacing your loan within the same bank.

Casual reminder that Refinancing refers to replacing your loan with another bank.

To really highlight the difference, I took the liberty of designing a few complex, multi-layered visuals to help with the comparison, which you can thank me for later.

Pie Chart

Bar Chart

Venn Diagram

Repricing vs Refinancing

I don’t think it’s exactly fair to say one is better than the other. They both have their merits, hence the reason why we’re even having this discussion. If it were that simple, the section would just be titled “Why Re_ is better than Re_”.

Instead, let’s look at it from another point of view.

While both Repri and Refi are good in their own right, their viability is affected by a few factors such as time, costs and eligibility.

Thus, instead of considering which one is better, let’s look at them which option is better for you at the point in time.

Time Required

Repricing takes a shorter time to process as compared to Refinancing.

This is because you’re staying with the same bank, and they would already have your details from when you first signed your loan with them.

Repricing a loan usually takes a few weeks.

Refinancing however, might sometimes even take a few months to finalize the loan. This is because you’re essentially a new customer, and it takes time to process the paperwork.

So, if you’re looking for an immediate option to change your loan (maybe because you were too busy to refinance earlier and now you kanchiong spider), repricing could be an alternative.

But wait, this is just the 1st factor ..

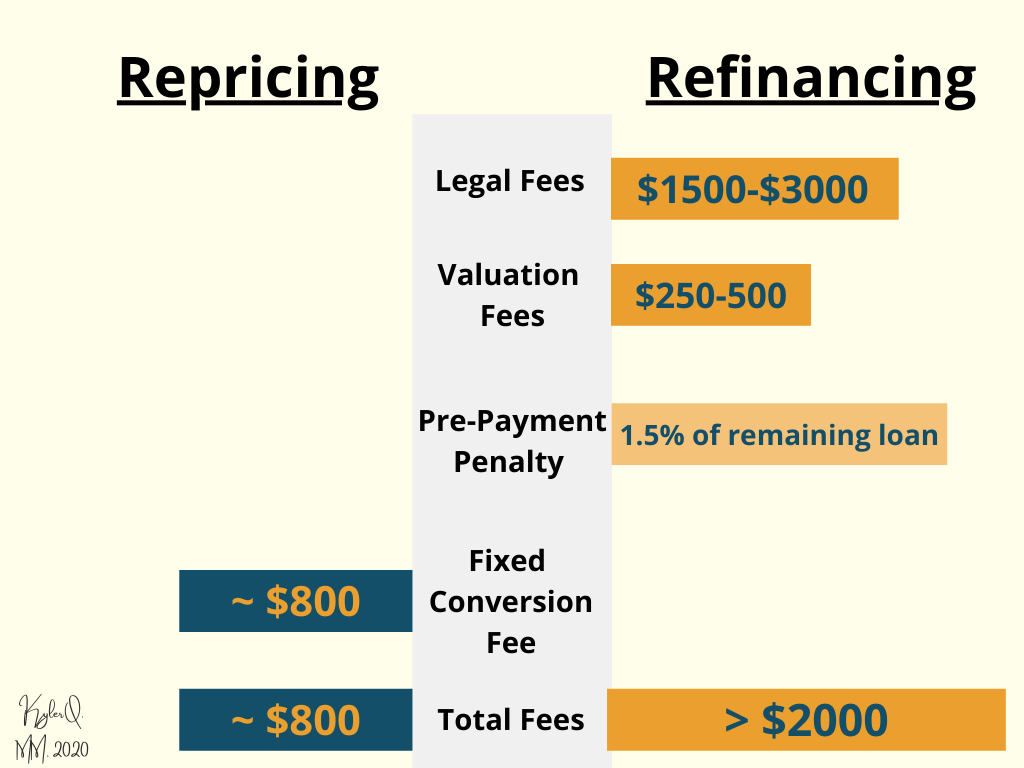

Costs Involved

Yes I know how it looks. You’re obviously siding with Repricing now because it’s the cheaper option.

But hold your horses, don’t be a victim of premature evaluation.

The reason why Refinancing has a higher incurred cost as compared to Repricing is because of the paperwork involved. This includes both legal fees and valuation fees.

Legal fees are what you pay your lawyer when you decide to switch the bank who’s financing your loan. This is a compulsory payment if you decide to refinance.

Valuation fees are what you pay to the bank, for their services on re-evaluating your loan. This is compulsory too as the bank has to assess your creditworthiness cause you know … will you lend someone money who you know can’t return it?

The Pre-Payment Penalty (or as I like to call it, 3P) refers to the fees you have to pay IF you decided to refinance during your lock-in period.

1.5% might seem small but 1.5% of a $400k loan is a straight-up payment of $6000.

Also I call it 3P because you confirm damn trippy and seh if you have the pay this cost

So if you don’t want to waste $6k, just … don’t … refinance … during … your lock-in period lul.

Needless to say, the costs above (Legal, Valuation, 3P) are only required if you refinance because it’s part of the process when you’re switching to another bank.

For repricing, only a Fixed Conversion Fee is needed for the administration of you switching from one loan to another.

That’s it.

Also, maybe this paints a clearer picture of how repricing is less time-consuming simply because there are less steps in the process.

So, if you’re looking for a more convenient process (maybe that month you kena from your boss until you just. can’t. anymore.), then repricing might be an option you can consider for your own sanity.

But wait, this is just the 2nd factor ..

Eligibility

Unfortunately, not everyone can refinance.

Typically, banks will not refinance loans for 2-room HDB flats or outstanding loans that have <$100,000 simply because it’s not profitable enough for them. These people only have the option to reprice.

So, if you happen to fall into either of these categories, repricing will be the way to go for you.

Having said that though, according to the 2019/2020 HDB annual report, the number of 2-room HDB flats makes up only about 2.63% of the total number of HDBs. That’s just a measly demographic and statistically speaking, this won’t affect the majority of you.

Your choices will only start to restrict as your balance is approaching the $100k amount.

So, logically, refinance whenever you can if you’re a new homeowner (of course only if interest rates are good AND you’ve cleared your lock-in period), and maybe look towards reprice after that.

Restoring the Reputation of Refinancing

I know that the majority of people who are actually in positions to repackage their housing loan are mostly working adults. And if there’s one thing I’ve learned since becoming one, is that nothing beats convenience.

I think this is especially accurate in our generation: the older we get, the more likely we’re willing to pay for convenience. And I’ve basically presented repricing as a super convenient option.

But please don’t forget the very reason why you’re even repacking your home loan.

It is to save money in the long run.

Repricing may save you time and incurred costs now, but refinancing rates are typically unbeatable in comparison.

Why?

Because the competitors of the bank you’re with are trying to win you over.

It’s literally that distracted boyfriend meme.

In an effort to zhut zhut you over to their side, they can offer some very enticing rates. And there’s nothing wrong if you decide to switch banks, I would do the same thing if I can save up to thousands on my mortgage loan.

If your refinancing admin costs are about $2400, but you’re able to save up $200 a month from a lower interest rate, it will only take you 1 year to “breakeven” and start saving. That is insane value!

So, don’t be too hasty to hop onto the repricing bandwagon. You may save a thousand now, but you can save on a few thousand more in the long run if you refinance.

Ultimately, it is more beneficial if we were to enter this phase with foresight and an open mind, and properly consider whether Repricing or Refinancing is the better option for you at that time.

Ok sign me up! But where do I start?

It’s honestly quite scary to decide on all these things.

I feel the same way as I’m entering adulthood and because of my work environment, I’m starting to think about my housing more and more each day.

(And I’m that type where I can barely decide what I want to get at McDonalds, and soon I’ll have to think about Repricing and Refinancing? I think I’m just gonna Rest in peace.)

So, if you do need to consult experts on which is the best route for you, don’t be shy to ask for some help!

There are wayyyyyyy more variables to consider such as your loan tenure, loan age, how much you’re left with on your loan ………………..

So really there’s no reason to geh kiang if you’re unfamiliar with these terms or you don’t know what’s the first step, that’s our job! All you gotta do is just drop us a call.

Or, if you’re more of a texter, just text us.

And if you can’t already tell from the contacting methods, it’s FREE to ask about anything you’re unsure of. No extra costs will appear on your phone bill, I promise you. (If have means you forgot to turn on wifi when you on youtube)

I think the most important factor is that you have to come into repackaging your home loan with the mindset of saving money.

I know everybody feels the pain of having to work your butts off to buy a house, then after that need to think of renovation la, when to visit your parents la, probably need to start thinking bout giving angbaos soon …. damn shag, so I think the least we can do is to help you save on some of the costs. (on the housing, not the angbaos)

Till next time, be good people.

Xp gained today: 77 (R=18,E=5,P=16,R18,I=9,C=3,E=5)

LEVEL UP!

Status: Lvl 2 Beginner

Tl;dr,

More in the WAT series

What are mortgage brokers and what the hell do they do? (WAT #1)