Welcome everyone, to a new series offering explanations on concepts/ideas/terms that are used in the property industry, by an intern with zero background in the property industry. Yep, you read that right.

In this series, I’ll be doing my best to explain these complex terms as simply as I can so that you can best understand it too. If you’re keen on learning more about the property industry, let’s go on this journey together. Welcome to the What Are They (WAT) series, by the Mortgage Noob in Mortgage Master.

Foreword from author:

Hey good lookin’, hope you’re having a fine day today. Full disclaimer for this article, yes I know mortgage brokers do refinancing & repurchasing too … BUT, please also understand that this is written for the purpose of sharing information with readers who are newer and might learn better with an easier example to relate to, hence I’m only using the example of new purchases/buying houses for this article. Mad love, take care, be a good person.

Let’s be frank here, the only time we’ve seen the word ‘mortgage’ is during the game of Monopoly. And even then, we don’t know what mortgaging in the game is actually supposed to do.

I’m not sure about you, but how I played was that when you’re short of money after purchasing properties (shoutout to my #TrafalgarSquarePeeps) and you need to pay for that daunting, sinister dark blue spot (edit: it’s Park Lane) that you just landed on, mortgaging the properties you owned seemed to be the only way to receive money in order to fund that rent you owed.

But is that exactly how it works in the real world?

What is a Mortgage Broker

Firstly, the term mortgage will only be used when it comes to the subject of Property. Property can apply to either residential (housing) or commercial (shophouses, building offices).

A mortgage refers to the loan you need to buy these properties that you desire.

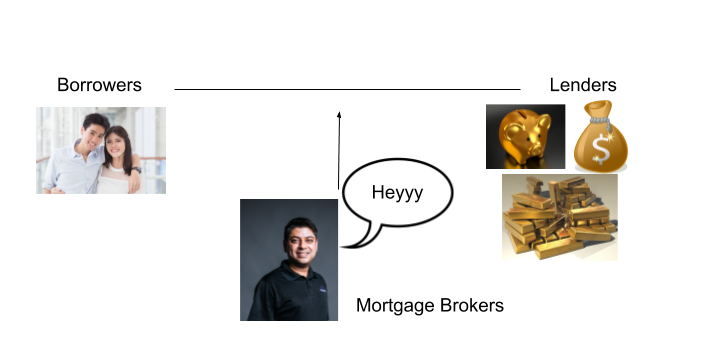

A mortgage broker is the “intermediary” who brings “borrowers” and “lenders” together.

Borrowers = people who need to borrow money to purchase a property (because they don’t have enough funds), and are typically made up of people such as you and myself. For example, if I’m interested in buying a house (which includes an HDB BTO), but I don’t have enough money to fully pay for it now, I’m a mortgage borrower.

Lenders = fund sources who have the financial capacity to loan you money. Typically, they consist of banks. Of course with different banks, comes different mortgage packages with different interest rates.

What does a mortgage broker do?

How the mortgage broker serves as an intermediary is to help gather information for a borrower and helps to assess which is the best route for them.

- This information includes which banks offer mortgage loans, their repayment model and their interest rates, among other things.

Essentially, they are the middleman between the people who want to buy a house but lack money, and the people who have the money.

Process of a Mortgage Loan

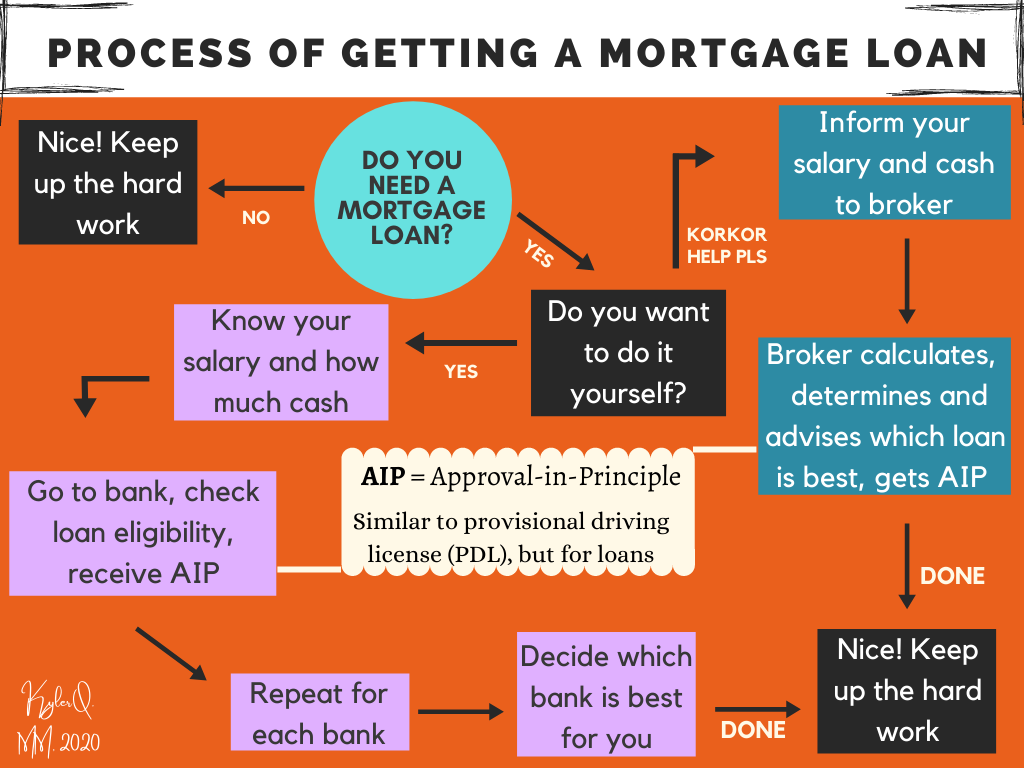

Now that you know what a mortgage broker is, allow me to further describe the general process of getting a mortgage first, before deciding whether you need one or not.

The first 2 steps of getting a house are typically

1. Researching and shortlisting houses

2. Picking your jaw off the ground after looking at the prices

After you’ve done that, you’ll have to ask yourself if you have enough money to set aside to purchase that house, or if you need a loan. If you do need a loan, you’ll need to decide whether you’ll want to do it yourself, or with the help of a mortgage broker.

You can see the route of using a mortgage broker helps to streamline what you need to do. They compare everything so you don’t have to, quickens the process, and essentially takes the stress off you. Furthermore, mortgage brokers are experienced in a sense that they’ve handled cases with varying degrees of income, so they would most likely know how to cater to your needs.

Of course, if you have the time to do your own research and enquire banks by yourself, kudos to you! You’re probably good on your own. It really does take effort to compile these numbers, and I commend you for that. However, this does bring me to my next point.

Do you even need a mortgage broker?

Well, that’s really up to you. Nobody can force you to consult a mortgage broker, but let me put it this way. Whether you need one or not depends if you rather spend time researching on your own, or save time when you have a mortgage broker do it for you.

If you need a more relatable example,

Your phone contract is coming to an end, and you plan to get a new phone. You have to research

1. different plans each telco offers

2. the extra money to pay upfront for that phone

3. how much data is in the plan

.

.

.

97. whether you can get a company discount or not.

How many tabs do you think you’ll have opened on Chrome? So … imagine someone compiling all this information, gathering the numbers and calculating them, and advising you on which route is best FOR YOU!

Needless to say, this is much more than getting a new phone that you just slapped a tempered glass screen protector on. This is a house that you’ll live in long-term. No such thing as changing it every 2-3 years. Additionally, there are way more numbers involved because for housing loans, it involves interest (I know you have none in this topic). That’s an article for another day (RIP me).

But I digress, the point I’m trying to get across is to let you know that getting a house is a HUGE commitment, and there are a lot of things to be considered before getting one. So, don’t be afraid to get some help if you need it. Furthermore, mortgage brokers can often get better rates because they directly bring clients to a trusted, reliable banker. So yay, more money saved.

How Mortgage Brokers earn money

I don’t know about you but the term ‘mortgage broker’ sounded very malicious when I first heard it. As if they’re out there to scam you for some reason? Is this just me? But maybe to offer you some security, how ‘bout I share about how they make their money with you?

Mortgage brokers and banks have already forged a relationship between them, like buddy-buddy but work wise. If the mortgage broker brings business to the banker, the banker earns commission for themselves, and the mortgage broker gets a referral fee.

Plus, mortgage brokers get the same amount of fee regardless of which bank you go to, allowing us to give free and unbiased opinions to marry the best loan to your financial situation.

But guess what … THAT’S NOT SOMETHING NEW!

It’s something we everyday people do as well! (ahem my friends who always give me shopee referral codes)

In fact, even influencers are getting referral fees whenever you quote {theirname10} on your purchase. So it’s definitely a common thing, and you can think of mortgage brokers as the influencers of the housing world. (just rmb to quote us too)

But what makes us Mortgage Masters?

Well, the way we do things are a little different.

Mortgage Master is built on the principle of our CEO, Mr David Baey, where there is a win-win-win-win (really win x4 this one) between customers-banks-bankers-brokers.

To break this down, let me illustrate how each party wins.

Who wins what and how

| Customers (you) | 1) Free consultations from us 2) Rebates if you refer your friend to us (you are the influencer now) |

|---|---|

| Brokers (us) | 1) Referral fees from banks when we assign clients to them |

| Bankers | 1) Commission for processing your home loan application |

| Banks | 1) Earn money from your monthly loan repayments |

So really, in our model, it’s winwin-win-win-win, where you not only win on FREE consultations, but you can also get money when you refer your friend to us*.

While we’re at it, if you are interested in finding out more about how Mr Baey came up with this model, do check out his article on the origins of it! (if you want to of course … not forcing, consent is the way to go).

Right now, it might seem too good to be true, especially if you’re new. Furthermore, those “GraPHiC dEsIGN is mY PASssIOn” posters at your lifts are telling you not to fall for scams (if you still think it’s one). But what’s the worst that can happen if you call us? It’s free, and if you decide that’s not for you, all you gave up was a few minutes concerning a decision that involves the next 30+ years.

With that, I hope you get a better and clearer understanding of what mortgage brokers are and what they really do. Of course, they are just one of the small aspects in this ecosystem that is the property industry, which I plan to cover in times to come. Do let me know too if you’re interested in any topics you wish to know more about. Till then, smell ya later fellow noobs.

P.S. If you’re still keen on finding out how mortgage works in Monopoly, find out below!

Also, if you read all the way till here, a massive thank you! You’ve started your journey on not staying a mortgage noob.

XP gained today: +26 (M=13, MM=26)

Status: Lvl 1 Beginner

TL;DR,

Monopoly Mortgage Rules

Ok now that the actual article is over, pretty sure I can be even more informal in my writing … let’s hope so, will lyk if my bosses scold me.

Anyway, so if you’ve played Monopoly, you’ll know that you receive the property card after you purchase it. For example, you purchase Trafalgar Square, you get the red property card that is the deed for that lot.

Now, if you step on another player’s property and you have to pay rent, BUT you don’t have enough money, what you can do is to mortgage your property. This means, you flip your property card over, and you get that amount of money stated there. Using the same example of Trafalgar Square, it’s $120 if I’m not wrong.

If it’s not sufficient, you have to mortgage more properties till you have enough money, or till you run out of properties and have to declare bankruptcy, whichever comes first.

If this $120 you receive from the bank is enough to pay off what you owe, carry on with the game.

If you’ve paid and survive, your property card stays flipped upside down – because you’ve mortgaged it. This means you technically don’t own it anymore, and that’s why you dont receive rent if other players land on it. How you can get it flipped back to normal, is to pay the bank the mortgage amount + 10%, and all is trafalgar square and dandy again.

Ok i’ve really ended now.