Singapore is a country where home ownership is so celebrated that many of us don’t want to just own one property. We love home ownership so much that we even want to own multiple properties. When you think of private property prices in Singapore over the years, a second property feels like a good investment.

As Singaporeans, we totally get this love for property. But over the years, owning a property in Singapore has slowly become less and less appealing since the days Singapore gained independence. In particular, the dream of owning multiple properties has become a much more expensive affair.

The Government has been introducing property cooling measures such as Seller Stamp Duty (SSD), Additional Buyer Stamp Duty (ABSD), Total Debt Servicing Ratio (TDSR) and Loan-To-Value (LTV) limit to discourage ownership of multiple properties.

The million dollar question in everyone’s mind is, is it still worth owning multiple properties in Singapore?

Let’s look at the arguments against and for owning a second property.

No, Owning A Second Property Is Not Worth It

1. 17% ABSD Is Just Too Much For A Second Property

The biggest hurdle to owning multiple properties in Singapore right now is the ABSD. The latest change to ABSD was in December 2021 where the ABSD was raised to 17% for Singaporeans who are buying your second property. For your third property, the ABSD is at an absurd rate of 25%. For Singapore PR, the ABSD rate is at 5% (first property), 25% (second property) and 30% (third property).

On top of having to fork out extra for your second property to pay off the ABSD, the real issue is that the ABSD isn’t reflected in your property’s valuation. This means that whatever amount you fork out to pay for ABSD, it will no longer be part of your net worth. To make things worse, the ABSD has to be paid in cash.

The reality is that having to pay 17% (or more) on top of your property’s valuation is simply an amount that is too much. There are better avenues of investing the 17% instead of paying for ABSD.

2. Property does not appreciate as much as it used to

Yes, properties are really good assets to own. It appreciates to help you beat inflation. In fact, the higher the inflation, the more your property valuation grows. On top of that, if you own a second property, you can use rental income to cover your mortgage payments.

But gone are the days when property prices in Singapore appreciated like they were strapped to a rocket. If you bought property in the 70s and 80s, for example, you could realistically sell them for 5 to 10 times the price today.

And while prices are still rising today, the truth is that we will never see such growth ever again in land scarce Singapore.

Some of us have become so overly fixated on owning properties that we fail to consider other assets such as gold, stocks, bonds and even crypto. Just because our parents have taken this property ownership route to becoming a millionaire, it doesn’t mean that it will work for us, especially when we no longer have the kind of windfall when selling our property.

Our inherited love for hard assets may be impeding our ability to think logically, blinding us to ignoring other investment opportunities.

Yes, Owning A Second Property Is The Way To Go

Like any good analysis, you need a balanced view that weighs the pros and cons of both side of the argument. There are three good reasons why owning a second property is still the way to go despite what we discussed above.

1. Singapore’s Property Market Is Resilient And Still Growing

One of the biggest concerns for property owners is that property valuation stops growing and plateaus. This is especially true for those of us who have a sizeable proportion of our net worth in one or two properties.

Despite recent gloomy forecasts, growth in property prices have yet to plateau. And the situation is quite the opposite. HDB prices have been climbing for 22 consecutive months up till May 2022. The same can be said for private properties where the private property index has trended upwards and scaling new all-time highs every quarter.

Source: Data.gov.sg

If Singapore can continue to keep its economy relevant to the global economy and stay competitive, we will continue to attract great companies and their talents to stay in Singapore. This will continue to drive the occupancy and ownership of properties and help keep our property market resilient. The more properties you own, the more you can benefit from the growth in hard asset prices.

2. Rental Income > Mortgage Repayment

If you are familiar with the famous “Rich Dad, Poor Dad” book by Robert Kiyosaki, you will know about the fundamental concept of Other People’s Money (OPM). According to Robert Kiyosaki, using OPM can help you increase the pace of your millionaire journey.

The fundamental idea behind OPM is to leverage debt and use it to earn more than what you are paying to the bank as interest. The classic example is to apply OPM on a second property. When you buy a second property, you will have one spare property which you can rent out. The rental income that you make on your spare property can then be used to cover the monthly mortgage repayment that you owe to the bank.

In some cases, you may even generate free cash flow that will give you additional monthly income to spend. After paying off your loan with the rental income, you get to own the property with just the initial upfront cost that you paid.

3. Keeping Mortgage Costs Low To Make Owning Second Property Sustainable

Apart from using rental income to cover your mortgage, there’s another way you can make owning a second property more sustainable, i.e. keep the cost of your mortgage low. That’s because the monthly interest payment that you need to make on your mortgage is quite sizeable.

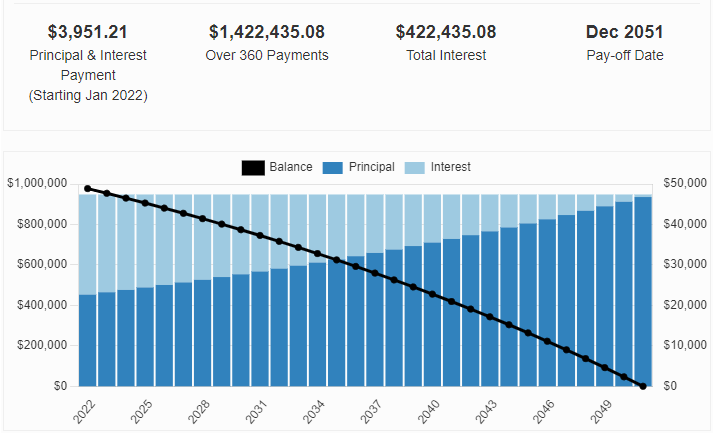

If you take a loan for $1M (at 2.5% interest rate) and repay the entire sum in 30 years’ time, the monthly repayments will add up to $1.422M. This means that over the lifetime of the loan, you would have paid $422k in interest.

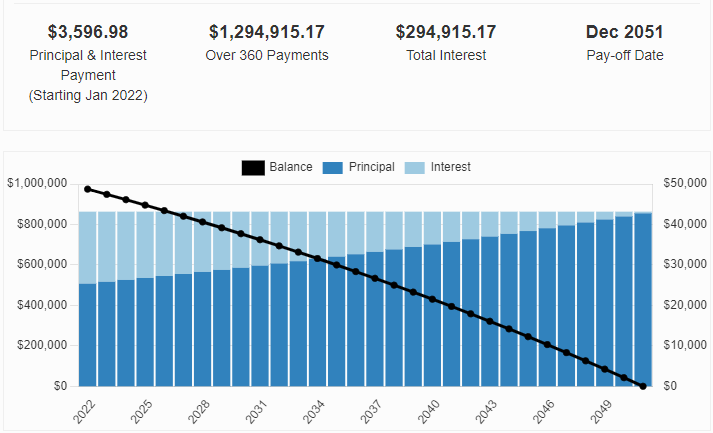

If you manage to reduce the interest rate to 1.8% by refinancing regularly, you will save over $100k on interest payment alone! That will reduce your cost of ownership of the second property by around 10%, which is a pretty big deal. This will help to make owning a second property less expensive while you continue to earn rental income off it.

Mortgage Master Is Here To Help Keep Your Mortgage Costs Low

Not sure how you can keep your mortgage affordable with the best home loan deals in town? Well, we get what you mean. That’s why Mortgage Master is here to help!

At Mortgage Master, we know the latest home loan packages in the market and sometimes can even offer exclusive interest rate packages that you cannot get directly from the bank. If you’re looking to purchase a new property, or refinance your existing home loan, fill up our enquiry form and our mortgage consultants will follow up with a call.