There are two types of home loans in the market- a HDB loan or bank loan. For HDB properties, you have the option of taking either a HDB or bank loan, but for private properties, you will only be able to get a bank loan.

Aside from deciding a loan that’s best for you, the next question is often whether or not you should pay using your Central Provident Fund (CPF) savings or cash.

Note: Only CPF funds from the CPF OA (Ordinary Account) can be used for home loan payments.

In this article, we will cover the following:

- Using CPF For Housing

- How Much CPF Can You Use?

- Advantages of Using CPF for Housing Loan Instalments

- Disadvantages of Using CPF for Housing Loan Installments

- Final Thoughts

Using CPF For Housing

You can use your CPF OA savings for your initial down payment, monthly repayments (for HDB and bank loans), stamp duties, and legal fees.

If you are buying a HDB flat, you can also use your CPF OA savings to pay the Home Protection Scheme (HPS) premium.

Note: For resale private property buyers, stamp duty is paid upfront by cash and reimbursed later by CPF. Do set aside enough cash before you exercise the option to purchase.

How Much CPF Can You Use?

This depends on the type of housing loan, property, and whether the remaining lease of the property can cover the youngest owner till 95 years old.

For a BTO with a HDB loan, there is no limit to how much CPF you can use.

For a condo with a bank loan, the limit is up to 120% of the property valuation. If the remaining lease is short, the percentage will be much lower.

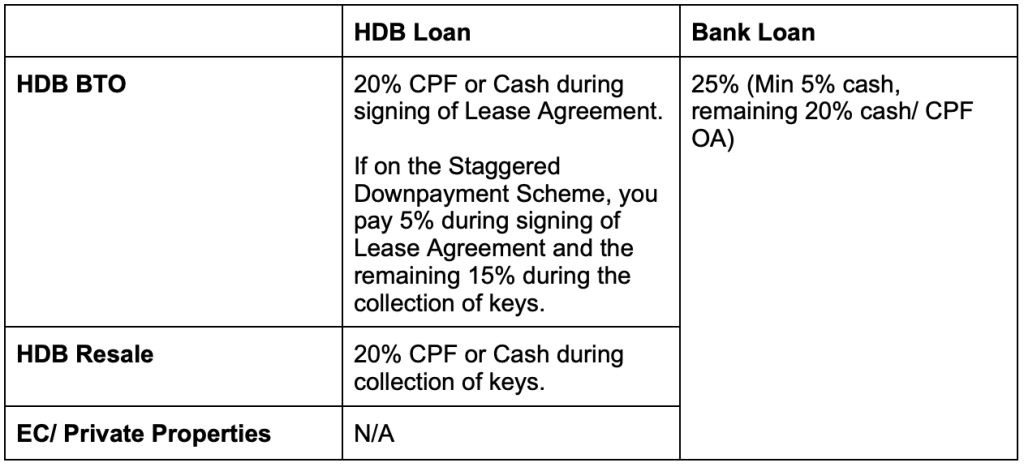

Downpayment Breakdown (HDB/ Bank Loan):

CPF Usage Limits:

When you buy a private property, your CPF usage is capped at 120% of the property’s Valuation Limit (VL). This is the lower of the purchase price or property valuation at purchase.

The Withdrawal Limit (WL) is the maximum CPF amount used for buying property, currently set at 120% of the VL. Your remaining mortgage payments must be serviced in cash.

CPF Withdrawal Limits:

- HDB loan for HDB BTO flat: No limit.

- HDB loan for HDB resale flat: Valuation Limit (VL), with potential to withdraw above VL up to the loan amount if CPF Basic Retirement Sum is met.

- Bank loan for BTO flat, resale flat, private property: Valuation limit, with potential to withdraw above VL up to Withdrawal Limit (120% of VL) if your CPF Basic Retirement Sum is met.

Note: All these are only applicable if the remaining lease can cover the youngest owner till 95 years old.

Retaining $20,000 in OA:

CPF also allows you to retain up to $20,000 in OA when taking a HDB loan. This provides a safety buffer for unforeseen circumstances like job loss, poor health, or inability to work.

Furthermore, CPF also offes an extra 1% interest rate for the first $20,000 in your OA balance, thus giving you a higher return.

Homebuyers with a bank loan can choose to preserve any amount in their OA savings. This means you can choose to not use any CPF, or wipe out your CPF, although retaining at least $20,000 is recommended for peace of mind.

Advantages of Using CPF for Housing Loan Instalments

1. Enhanced Liquidity with More Cash on Hand

Utilizing CPF for your home loan allows you to keep a larger portion of your salary for other expenses. This frees up cash for various aspects of your life, such as renovations, furnishings, bills, vacations, and medical emergencies. In contrast, repaying with cash reduces the money available for other household essentials. Additionally, you can invest this liquid cash in opportunities like REITs, stocks, forex, and cryptocurrency, potentially yielding higher returns.

2. Predictable Housing Loan Expenditure

Opting for an HDB Loan with a stable long-term interest rate enables better financial planning. Unlike fluctuating bank rates, the HDB loan rate has been consistently at 2.6% for years and is likely to remain stable until CPF interest rate revisions occur.

This stability allows you to calculate your housing expenditure at a stable 2.6% interest rate, regardless of market volatility.

3. Utilize CPF for Home Loans During Retirement

You can continue using CPF for home repayments after the age of 55, preserving your personal savings for other retirement-related expenses.

Your CPF payouts will come from your CPF Retirement Account (RA), which comprises funds from your CPF Special Account (SA) and CPF Ordinary Account (OA) until the full retirement sum is reached. Home loan repayments can still be made from the remaining balance in your CPF Ordinary Account, or you can choose to use cash after turning 55.

Disadvantages of Using CPF for Housing Loan Installments

1. Impact on Future CPF Retirement Savings

Using CPF for your housing loan depletes the compounding power of your CPF funds, affecting future retirement savings and payouts.

For those relying solely on CPF for retirement or following the 1M65 movement, cash payments for home loans are advisable. In a low-interest environment, finding a risk-free investment with returns higher than CPF OA’s 2.5% is challenging.

Only consider withdrawing from CPF if you are actively investing in higher-return instruments at an acceptable risk level.

2. Refund with Accrued Interest Upon Property Sale

Homeowners must refund the full CPF amount used for property purchase along with accrued interest (currently 2.5% a year). The longer the CPF funds are out of the account, the more you’ll need to refund upon selling the property.

This refund can be used for your next property or retirement needs. Accrued interest on CPF funds and home loans can accumulate quickly, especially with rising mortgage rates. Home sale proceeds first cover the outstanding loan, followed by the CPF refund.

If sale proceeds fall short, resulting in a “negative cash sale,” you must top-up the CPF refund difference in cash, out of pocket, if the property is sold at a loss.

Optimizing your CPF usage for housing loans involves balancing liquidity, investment opportunities, and future retirement savings. Understanding the advantages and disadvantages ensures informed financial decisions for long-term stability.

Final Thoughts on CPF Payments for Housing Loans

Using CPF funds for your housing loan payments is convenient, but it also leads to accrued interest that you’ll need to repay later.

At Mortgage Master, we prioritize financial prudence. Our expert mortgage consultants provide the best advice on how to allocate CPF and cash for your home loan repayments based on your financial health.