%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20451.277%20451.277'%20style='enable-background:new%200%200%20451.277%20451.277;'%20xml:space='preserve'%3e%3ccircle%20style='fill:%23334D5C;'%20cx='225.638'%20cy='225.638'%20r='225.638'/%3e%3cpath%20style='opacity:0.1;enable-background:new%20;'%20d='M450.975,237.605l-96.054-96.054H96.355v168.173l141.25,141.25%20C352.705,444.96,444.96,352.704,450.975,237.605z'/%3e%3crect%20x='96.353'%20y='141.553'%20style='fill:%23F6C358;'%20width='258.56'%20height='168.172'/%3e%3cpolygon%20style='fill:%23FCD462;'%20points='225.638,210.645%20354.921,309.725%2096.355,309.725%20'/%3e%3cpolygon%20style='fill:%23DC8744;'%20points='225.638,249.791%2096.355,141.552%20354.921,141.552%20'/%3e%3cpolygon%20style='fill:%23FCD462;'%20points='225.638,240.631%2096.355,141.552%20354.921,141.552%20'/%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3cg%3e%3c/g%3e%3c/svg%3e)

If you’ve been doom-scrolling the news about the Iran conflict lately, I bet your first thought was: “Great, there goes my home loan.” It’s a natural reaction. Most people assume war equals expensive oil, which equals inflation, which means the banks are going to hike your interest rates.

It sounds like a logical chain of events, but if you look at how the global economy has actually behaved over the last 30 years, that "logic" is almost always wrong.

At Mortgage Master, we don't just look at the surface-level headlines. We dig into the data that actually moves the needle for your monthly installments. While everyone else is reacting out of fear, let’s talk about why this conflict might actually make your mortgage cheaper in the long run.

The "War Bond" Myth

Back in 1945, countries funded wars by issuing "war bonds," which sucked cash out of the economy and pushed interest rates up. We haven’t seen a major war bond since WWII. In the modern world, rates don't move because of soldiers; they move because of economic cycles.

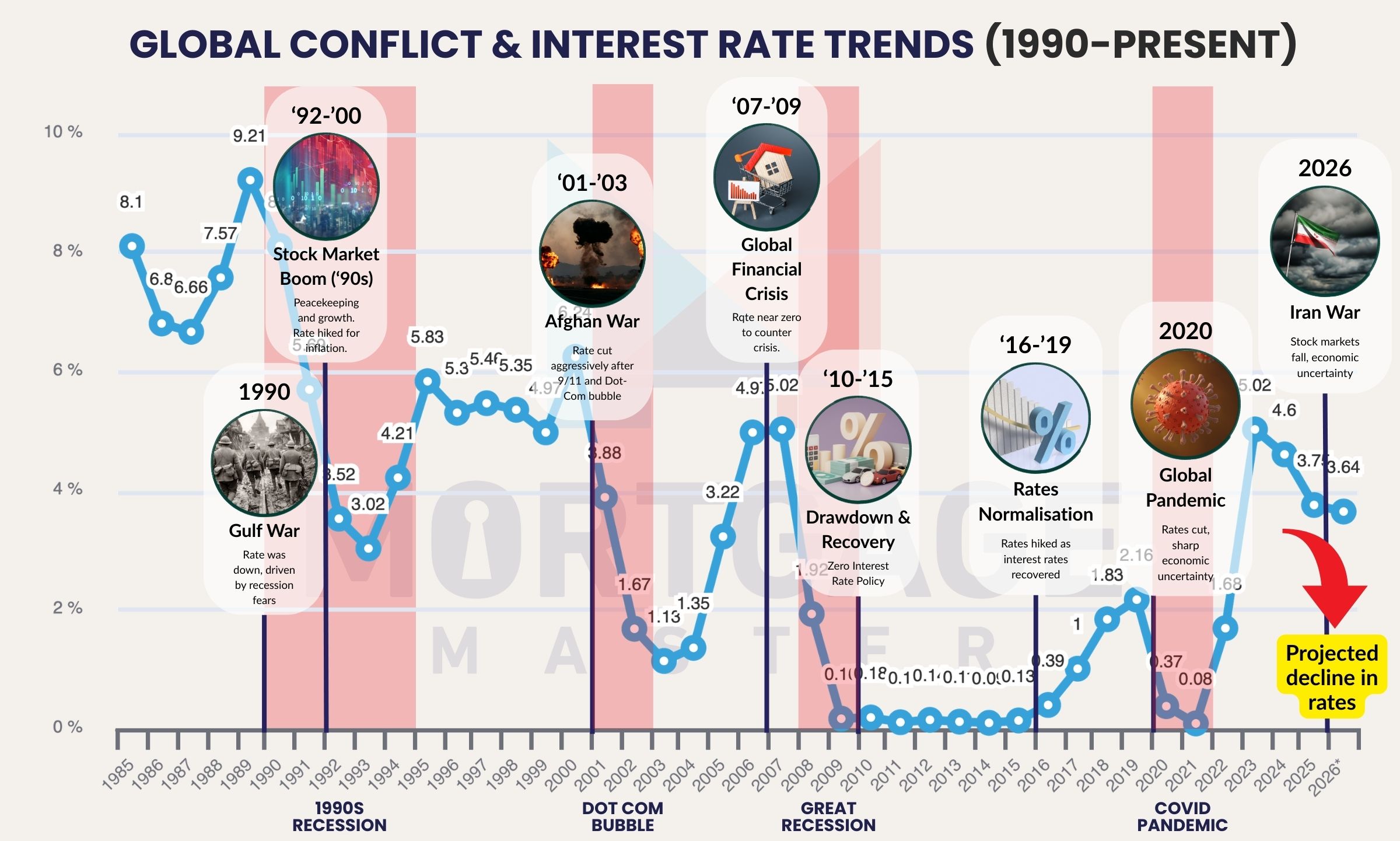

Relooking Our Historical Data (1990–Present)

We pulled the numbers from every major military milestone since 1990 to see what actually happens to rates when the shooting starts. Aside from the unique "perfect storm" of the post-pandemic recovery in 2022, the pattern is surprisingly consistent: conflict usually ends in a rate cut.

The 6-Month "Flip"

Here’s the reality of how these things play out. In the first 90 days, the "layman’s logic" is usually right. You’ll see a knee-jerk reaction: oil goes up, which has a trickle to make everything expensive, especially everyday essentials like your groceries. Logistics companies also start adding "war surcharges" to everything.

But give it six months, and the "Recession Effect" kicks in.

War makes investors nervous. They stop spending and start hoarding cash in "safe-haven" assets like government bonds. When billions of dollars pour into bonds, the interest rates on those bonds, and eventually the mortgage rates linked to them, start to slide. Effectively, war becomes a trigger for an economic slowdown, and the only way for central banks to fight that is to lower interest rates.

The Verdict: Don't Lock Yourself In Out of Fear

It’s tempting to run to the nearest bank and lock in a high fixed rate because you’re afraid of the "War Effect." But history shows that every major modern conflict has eventually caused interest rates to decline, not rise.

If you’re looking at your mortgage for the next 2 to 3 years, the smartest move is often to stay flexible. Floating rates (linked to SORA) allow you to capture the downward trend once the initial "knee-jerk" inflation of the war passes.

Worried about your upcoming home loan renewal? Reach out to any of our mortgage brokers who can run the numbers and help you see if a floating rate is the right move for your home loan.