When it comes to mortgages, timing isn’t just important — it’s everything. Lock in a loan at the wrong time, and you could be stuck paying tens of thousands more over the next few years. But catch the cycle just right? You could be saving serious money while everyone else scrambles to refinance.

That’s why understanding the interest rate cycle is no longer optional. It’s essential. Especially right now, as the tide begins to turn.

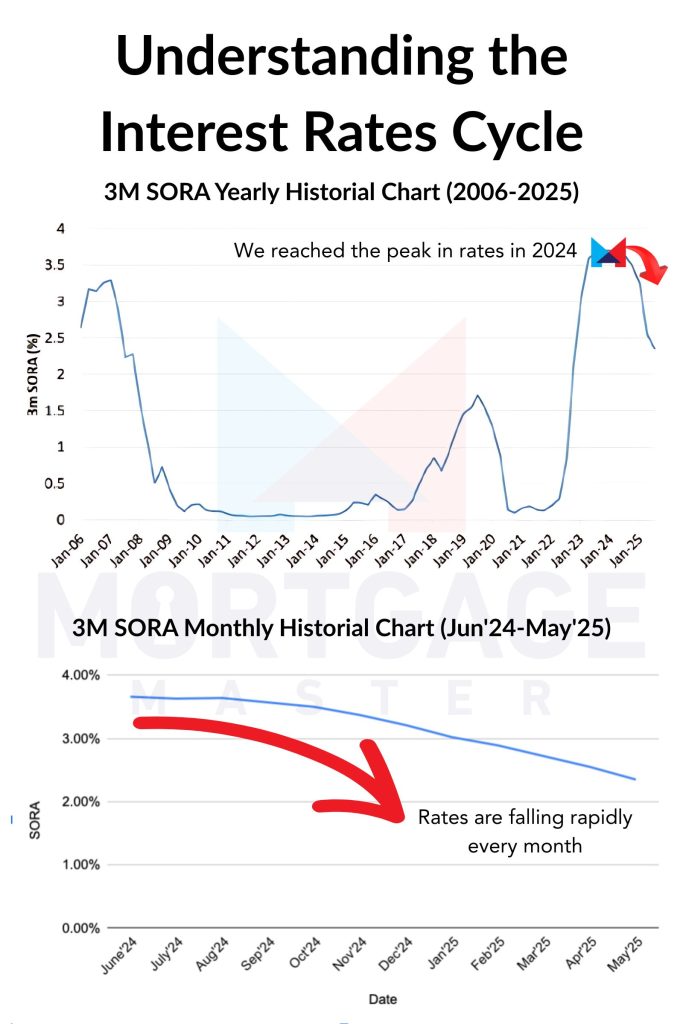

What Is the Interest Rate Cycle?

In simple terms, interest rates don’t stay still. They rise when central banks want to slow inflation, and fall when the economy needs a boost. This rise and fall, like a wave, is what economists call the interest rate cycle.

In Singapore, the 3-Month SORA (Singapore Overnight Rate Average) is the key benchmark rate used to price most floating rate home loans. When inflation runs high, MAS tightens monetary policy to slow things down. When inflation is under control, they start easing again, and that’s when interest rates start falling.

Where Are We Now in the Cycle?

Let’s look at the facts:

- In January 2025, MAS loosened its monetary policy — the first time it’s done so in years. This is a clear signal that the fight against inflation is easing.

- In April 2025, analysts interviewed by CNA said they expect further easing in the months ahead.

This isn’t speculation. It’s the natural rhythm of the market — and we’re seeing unmistakable signs that we’re heading into a falling rate environment.

The Window of Opportunity That Most People Miss

On paper, fixed rates today may look more attractive — 2.40% fixed vs. 2.65% floating (3M SORA + 0.25%). Most people would pick the lower number without question.

But here’s where smarter borrowers zoom out and look at the full picture: Where are interest rates heading next?

The writing’s on the wall — SORA has already softened from its peak, and with more monetary easing on the horizon, we could be staring at 2.0%, 1.8%, or even 1.5% by next year.

And if that happens?

Your floating rate starts to automatically decline. Your interest payments shrink without you lifting a finger.

That fixed rate? Stuck where it is.

This is what we call strategic positioning — taking a slight hit now (e.g. paying $80 more a month), in exchange for potentially four-digit savings every year when the rates come down.

Timing Is Everything — And It’s Not as Simple as Waiting

Some say, “I’ll wait till SORA drops, then I’ll switch to floating.”

But here’s the insider truth: banks adjust their margins fast.

When rates are high, banks offer thin spreads like +0.25% to attract borrowers. But once SORA drops, they widen the spread — sometimes as high as +0.80%. And just like that, the package you were eyeing isn’t so attractive anymore.

By then, you’re too late. The golden opportunity has passed.

Want to Play It Smart? Get the Right Strategy.

Anyone can quote you a rate. But not everyone understands when to act — and why.

At Mortgage Master, we’ve studied interest rate cycles inside out. We only recommend floating at one very specific point: just before the decline.

That point is now.

We’re not afraid to say what others won’t: Floating beats fixed — if you know when to use it.

Let us help you think 3 steps ahead. Book a free consultation call today and find out exactly how much you stand to gain, and how to make your next mortgage move with confidence.