Understanding your property valuation is important when you are looking to buy or sell your current home.

Understanding Property Valuation

A property valuation is typically carried out by a licensed appraiser and is an assessment of what your property is worth.

There are two kinds of valuations, indicative and actual valuations.

Indicative Valuations

Indicative Valuations are basic estimates of a property’s value.

It is usually based on the average price of similar recently transacted properties in the same area. Both homeowners and agents can perform these valuations through simple research.

However, these days, most people rely on free online valuation tools generated using AI to get an indicative valuation of their property.

Actual valuations

Actual valuations are performed by qualified surveyors and valuers and are much more detailed in nature. They are usually engaged by HDB (if you are buying or selling your HDB flat), by buyers after issuance of OTP, or by the banks (if you are taking a bank loan).

Oftentimes, there will be variations between the indicative and actual valuation due to the thoroughness of the latter. Your actual valuation will also be what HDB or the bank will look at when deciding the amount of loan you can get for the property.

What goes into an official property valuation?

Every licensed appraiser has their own method in generating the actual valuation of your property. The actual calculation remains a trade secret, but some will share that these are some of the factors they look at:

Location

This includes current and future amenities of the area, how accessible it is, how congested traffic is etc.

Price Trends

What were the recently transacted prices of nearby properties.

Property Characteristics

The bigger the property, the higher the value. Additionally, the floor you live on, facing of property, number of rooms and layout also affects the valuation.

Current Conditions

This includes the overall state of the property, type of finishing used, how recently renovated it was etc.

Rental Yield

How much similar properties in the area were rented out for.

Block and Facing

Which block your property is at, how much light and heat comes in, the kind of view you have.

Remaining Lease

Whether it is a freehold or leasehold property, and how many years of lease is left.

Because of the thoroughness of their assessment, a licensed appraiser can generate a valuation that is wildly different from the indicative valuation you got. It is also possible for different appraisers to generate different values as they may place different importance to different factors.

Additionally, depending on the purpose of valuation, the final amount will also be different. A valuer engaged by the seller to get the fair market value of the property may generate a different valuation from one engaged by the bank to determine the amount of mortgage to loan out for the property.

As a buyer, you can request for a valuation report with the breakdown in an appraiser’s assessment of the different factors. The best way to get an accurate price indication is to seek valuation quotes from multiple appraisers (We recommend up to three.) and take the one with the majority range.

You can get a valuation report directly from HDB who will typically get one of their panel of valuers to head down to your HDB unit to assess its value.

For homeowners looking to sell, you can engage your own valuer from the Singapore Institute of Surveyors and Valuers (SISV) to get a “fair value” of your property. If you have an agent, your agent might also be able to recommend someone reliable.

For buyers, you will need to go through your bank to get an official valuation if you are getting a private property. If you are buying a HDB, you will still need to go through HDB valuation, regardless of whether you are taking a HDB or bank loan. You should also note that the official valuation is done after mortgage approval.

Banks will base their loan on the indicative valuation to approve the mortgage, but also reserve the right to revise the loan amount if the official valuation amount differs.

For buyers, you will need to go through your bank to get an official valuation before your mortgage can be approved for your private property. If you are buying a HDB, you will still need to go through HDB valuation, regardless of whether you are taking a HDB or bank loan.

Do note in most cases, you will need to pay the valuation yourself unless there is a subsidy from the bank. Banks typically provide subsidies for refinancing and not a new purchase.

If you are buying a HDB, HDB’s valuation fee sits at $120. A bank’s valuation fee would depend on the property type, price and status. It typically ranges between $100 to $5000.

Advantages of getting a property valuation for sellers

Getting a proper valuation done will help homeowners price their properties more accurately for sale. You do not want to underprice your property and miss out on possible gains. Alternately, you do not want to overprice it too much and not get any offers at all.

Other additional perks of getting a proper valuation done includes:

Giving potential buyers a peace of mind as it shows them the “fair value” of your property.

Minimize disruptions to completion of sale as any COV that is needed will not catch your buyers off guard.

Not underpricing your properties and getting into unnecessary price disputes with buyers.

Property Taxes

When purchasing a property in Singapore, you will need to pay Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD). This amount is applied to the property price or valuation, whichever is higher.

If the price of the property is $2.5mil but your valuation report indicates a value of $2mil, you will still need to pay BSD on $2.5mil.

You can calculate your BSD from this table:

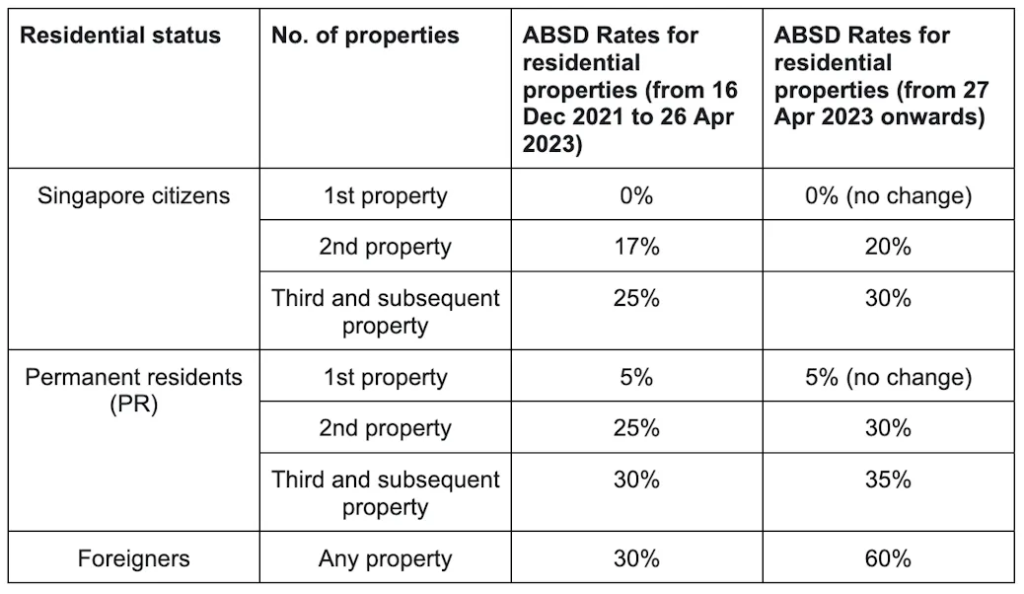

Additionally, if you are buying a second property, or are a foreigner, you will need to pay ABSD:

Your BSD or ABSD will always be based on the property price or valuation, whichever is higher. This is why having a valuation match closely to the price of property is important for buyers.

Buyer Affordability

The actual valuation of the property can vastly differ from the original indicative valuation. With higher price comes higher costs, and this reduces the pool of buyers who can afford your property.

CPF Withdrawal Limit

If you are looking to use your CPF to buy your property, you will need to take note of the CPF withdrawal limit. It is currently set at 120% of the property price or valuation, whichever is lower.

For example, if your property is priced at $1mil, you will only be able to use up to $1.2mil of your CPF to pay for it. These include your stamp duties, legal fees, and other property purchase related fees.

Getting the best loan

At the end of the day, your bank’s valuation ties in closely with the loan you can get. In order to get the best loan, consider engaging a mortgage broker like us who can help. Due to our existing relationships with banks, our brokers will be able to get information from multiple banks and present you with the best loan for your property.

Furthermore, our services are free and we guarantee the best rates there are in the market.